"The cost of waiting isn't zero, it just doesn't show up on a statement?"

Most people think there's no point to working with a financial advisor, or they may think that they don't have enough money to work with one, but are those good reasons?

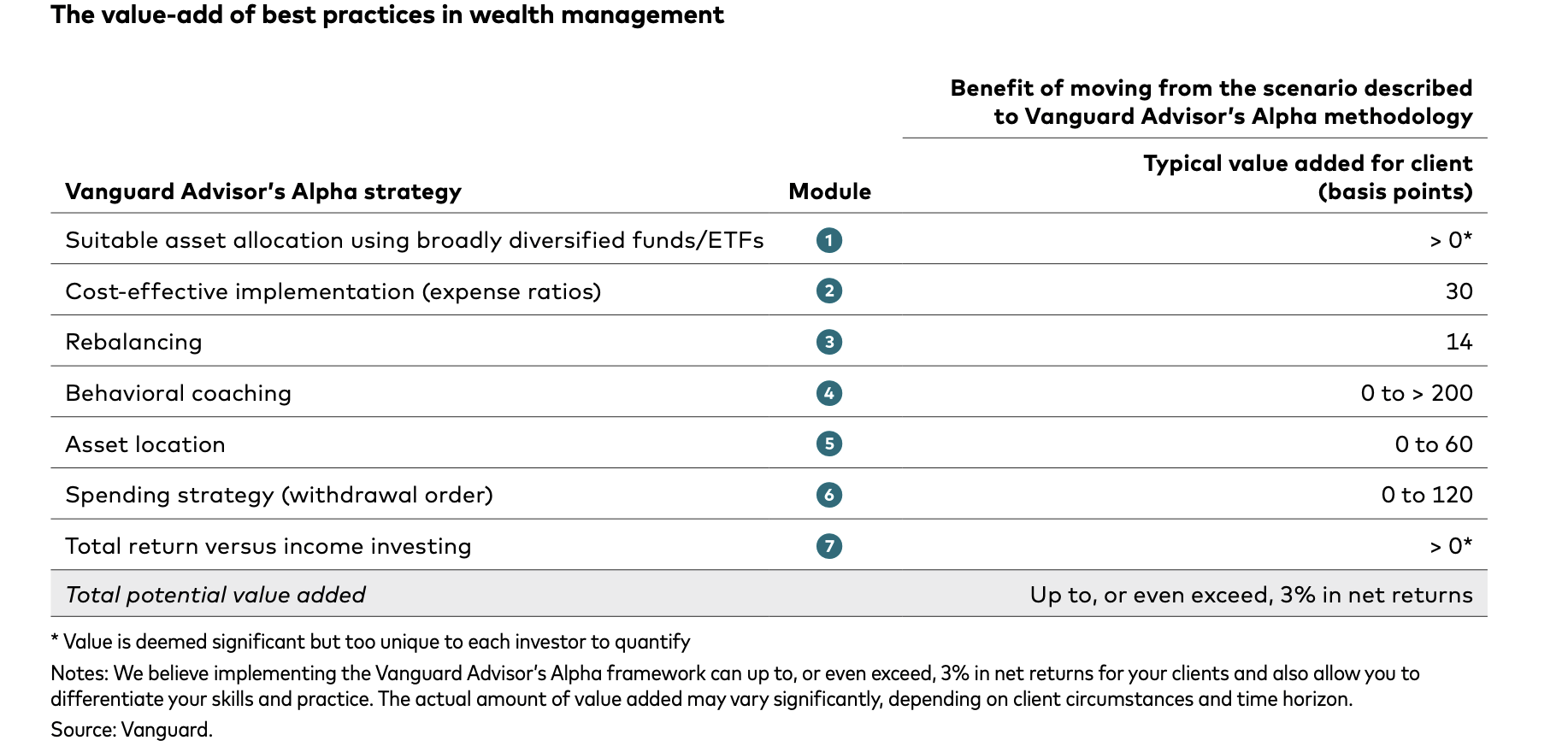

It's well documented that Vanguard conducted a study and has put a 3% annual return increase on those who work with a financial advisor over those who don't. Check out our blog on that here.

Not having enough money may be true with some advisors, but many advisors, including us at HFP, have no minimum to work with us. The industry as a whole is beginning to move towards little or no asset minimums.

So if working with an advisor gives better returns and the barriers to entry are so low, then the question becomes when should you work with an advisor?

When to work with a financial advisor

TRIGGER #1 — YOU GOT A REAL JOB AND HAVE A 401K YOU DON'T UNDERSTAND

-Most people just pick a target date fund and forget about it — which isn't the worst thing, but it's not a plan. These funds have high fees that can cost you thousands and little flexibility to meet your unique needs. Check out our YouTube video on them here.

-Contribution rate, employer match, Roth vs. traditional — these decisions made early have enormous long-term consequences

-This is usually the first moment where a one-time flat fee conversation actually pays for itself many times over

-You typically don't need ongoing management at 28 - you might just need someone to set you on the right direction.

TRIGGER #2 — YOUR FINANCIAL LIFE GETS COMPLICATED

-Marriage: combining finances, beneficiary updates, insurance review — a lot of moving pieces that people just don't get around to

-Kids: 529 accounts, life insurance, updating your will — most couples with young kids have completely inadequate estate plans

-Buying a home: how does this change your cash flow, your emergency fund, your retirement savings rate?

-Any one of these three is a good reason, but all three at once means you can really reap benefits from working with an advisor.

TRIGGER #3 — YOU'RE HITTING YOUR PEAK EARNING YEARS

-Roughly 40s-50s — income is up, expenses may be stabilizing, retirement is close enough to feel real

-This is when tax planning really starts to matter — marginal rates are higher, so every dollar of smart tax strategy is worth more

-This is also when people start accumulating real assets — and making real mistakes with them

-Concentrated stock positions, stock options, deferred comp — these are genuinely complex and the cost of getting them wrong is high

TRIGGER #4 — SOMETHING CHANGED

-Inheritance: sudden influx of assets, potentially complex tax situation, emotional decision-making at the worst possible time

-Divorce: QDROs, splitting retirement accounts, rebuilding a financial plan from scratch — genuinely one of the most financially dangerous life events

-Job loss or early retirement offer: do the math before you make the decision, not after

-Death of a spouse: survivor benefits, Social Security timing, portfolio restructuring. People make permanent decisions in a really vulnerable state

-Many of these moments are where emotions and finance combines, and where it is very important to have an impartial advisor helping you decide.

TRIGGER #5 — RETIREMENT IS WITHIN 10 YEARS

-This is the red zone — the decisions made in the last decade before retirement have an outsized impact on outcomes

-Sequence of returns risk: a bad market in the first few years of retirement can permanently impair a portfolio even if it recovers later

-Social Security timing: claiming at 62 vs. 70 can mean a difference of $100,000+ in lifetime benefits depending on the situation

-Medicare, withdrawal sequencing, Roth conversions before RMDs kick in — this stuff is complex and the stakes are high

Want to Know If Your situation needs an Advisor?

We're fee-only CFP® advisors in Austin, TX, specializing in financial plans and asset management for clients nearing retirement. Schedule a free call and let's look at the real numbers.

Schedule A Free Call

ULTIMATELY

You don't need to be rich to need a financial advisor — you need to have decisions in front of you that have real consequences

The cost of waiting isn't zero — it just doesn't show up on a statement

Thanks for reading

FAQ

Sources and recent readings:

Recent blog:

https://hamiltonfinancialplanning.com/blog/inflation-the-silent-killer/

Vanguard 3% study:

https://www.vanguardsouthamerica.com/content/dam/intl/americas/documents/latam/en/2022/08/mx-sa-2335954-putting-a-value-on-your-value-quantifying-vanguard-advisors-alpha.pdf

If you have any questions head to HamiltonFinancialPlanning.com to find out more and schedule a free call with our fee only CFP fiduciary advisors who specialize in building financial plans and investment management for clients nearing retirement in Austin and Houston TX.

Scott Hamilton is founder and chief financial officer at Hamilton Financial Planning, a wealth management firm that specializes in providing comprehensive financial planning for retirees. With over 20 years of experience in the financial industry, and having completed over 250 financial plans for retirees across all industries, Scott is passionate about providing his clients with the tools and insight they need to achieve their financial goals. He has a Bachelor of Business Administration in finance from Texas State University and an MBA in international finance from Pepperdine University. Scott has also been happily married to his wife, Gayle, for over 25 years. To learn more about Scott, connect with him on LinkedIn.