After working for a lifetime and saving into qualified pre-tax accounts (Like 401(k) and Traditional IRA) you now realize that rolling some or all of that amount into a Roth could be better for your overall retirement and saving goals. Now that you’ve figured that out, then the next logical question is, how should you go about converting this?

Table of Contents

What is it?

A conversion like this takes all of the money out of these qualified accounts and puts it into your income, meaning you will have to pay income tax on that amount as if it were earned income from working. This Inclusion into taxable income creates some problems.

Problem this could pose

Having a high income is a great thing, but having a high taxable income can be a big problem.

Increases income

For one thing if you’re still working then doing these rollovers will be like having another income source, and will push your tax bracket up higher. If your taxes are already high on one income, the idea of having another income source taxed may not be so appealing.

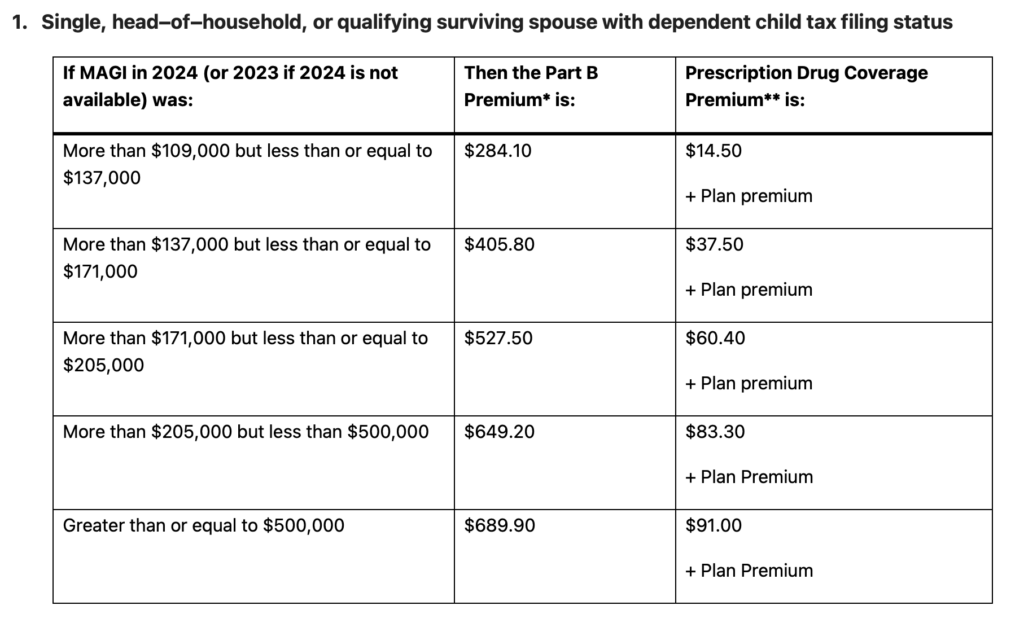

IRMAA Surcharges

If you’re currently receiving Medicare and making premium payments, the increased income from these conversions will impact your premiums and IRMAA (Income-Related Monthly Adjustment Amount), a surcharge that is added onto high earners’ Medicare premiums, with the upper limits being an extra $487 a month ($5,760 per year – $11,520 for married).

Keep in mind this surcharge is in addition to the ordinary income tax you will already be paying. Even one dollar over the income limit will increase this surcharge and cost you big.

Social Security Tax

If you’re taking Social Security, know that up to 85% of it can be taxed for the higher earners. If your Roth conversions are too high in one year, then you can easily rise above the threshold and face that 85% rate.

Some ways to work around this exist though.

Often you can strategically convert only set amounts of the retirement account. By only converting portions of it in a year you can reduce the amount of taxable income that you have for that year, and work to stay below the tax bracket, Social Security, and IRMAA tax limits.

Really, your most powerful tool for these conversions is timing and amount. You will have to pay taxes on any amount that you convert, but how much tax you pay and when you pay it can both be controlled for. You should try to do these conversions in low earning years, where your total income will be the lowest.

Working with a financial advisor, we have tools that simplify this process and make it clear which options you have that produce the best outcome for you.

If you have any questions head to HamiltonFinancialPlanning.com to find out more and schedule a free call with our fee only CFP fiduciary advisors who specialize in building financial plans and investment management for clients nearing retirement in Austin and Houston TX.

About Scott

Scott Hamilton is founder and chief financial officer at Hamilton Financial Planning, a wealth management firm that specializes in providing comprehensive financial planning for retirees. With over 20 years of experience in the financial industry, and having completed over 250 financial plans for retirees across all industries, but mostly the oil and gas industry, Scott is passionate about providing his clients with the tools and insight they need to achieve their financial goals. He has a Bachelor of Business Administration in finance from Texas State University and an MBA in international finance from Pepperdine University. Scott has also been happily married to his wife, Gayle, for over 25 years. To learn more about Scott, connect with him on LinkedIn.